Our just-in-time global system is engineered for economic efficiency, but with little ‘fat’ in the system, it is very brittle. The current supply chain disruptions are about to give that system a brutal kick that will have cascading effects throughout the global economy, some of which are predictable and some will come as a shock. One of the most predictable is disruption of the food supply, as supply chains for both fuel and fertiliser are heavily impacted by the war. Such disruptions cause famines, as they have throughout history. In the northern hemisphere, the window for planting is likely to be missed, and in the southern hemisphere harvest and distribution are likely to be substantially disrupted.

Demand shocks from panic buying tend to be short-lived, but supply shocks are not. They cause long-lasting shortages that must be adapted to. People are going to have to tighten their belts, become as productive as possible, and as collectively creative as possible. Access to productive land is necessary, but that need not imply ownership. Farmers deprived of fuel for machinery are going to be needing human labour, and labour will be exchanged for food. Urban ‘victory gardens’, as practiced in the UK during the WW2 blockade, are also possible, and essential. Food storage will matter a great deal, so learning various techniques for preservation is important.

Knowing what to store matters as much as knowing how. Proteins and fats are essential nutrients, but carbohydrates are not. They’re easier to store, but nutritionally insufficient. In addition, high glycemic index carbonydrates spike blood sugar, cause insulin secretion, which crashes blood sugar, resulting in sugar withdrawal that feels like intense hunger. This means you can be causing hunger by eating the wrong things. If blood sugar is stable, hunger is less urgent. Of course proteins and fats are more expensive and more challenging to store. It would be worth looking up recipes for pemmican, which is a travel food relied on by native people’s in North America. It’s not a taste treat, but it is an excellent survival food, and doesn’t require complicated storage.

Collective action will be essential. Communities will need to organise soup kitchens, involving local supplies and volunteer staffing. Cooperation can keep people fed, and is infinitely better than every man for himself, which would mean pointless conflict and thievery. The mindset shown at the anti-mandate demonstration at the Wellington Parliament is exactly what’s needed. People spontaneously organised a small village in a matter of days, and it functioned extremely well, all based on volunteering, donations, and cooperation.

Having hard goods for barter would be a great asset, but relative values will have changed dramatically. If you’re hungry enough, an ounce of gold may be worth half a dozen eggs and a loaf of bread. Tools, liquor, cigarettes, soap, coffee, and other practical goods that are currently not particularly expensive might make much better trading goods in an energy constrained future. Practical skills can also be traded, perhaps within a timebank structure, and even entertainment can be worth a meal. Introducing alternative forms of liquidity during the coming economic depression, such as local currencies, can make major difference, as that can alleviate some difficulties by facilitating trade between producers and consumers. The official form of purchasing power is likely to be in short supply in depressionary times, hence the need to supplement it.

Depending on location, the impact on the food supply could begin with distribution, meaning that food has been grown, but cannot be harvested and delivered due to fuel constraints, so shelves empty quickly. In other places, planting may be possible, but with insufficient fertiliser yields would be much smaller, and the impact may be compounded by insufficient fuel later in the cycle. Impacts will be uneven, as circumstances will be highly variable. Cities will fare worse than rural areas. Productive skills will matter more than almost anything, and neighbours must help each other. The coming shock could be the largest in human history, coming at a time when people are very poorly prepared to face it compared to historical examples. Cohesive communities are the way forward, and resilience must be relearned.

Australia and New Zealand lie at the far end of the long and vulnerable supply chains of a globalised world. The energy crisis hitting primarily Asia, due to its overwhelming dependence on the oil and LNG from the Straits of Hormuz, will hit Australia and New Zealand region even harder, since they’re our direct suppliers, and Asian countries will naturally prioritise their own economies before allowing exports of scarce resources. Both Australia and New Zealand have greatly reduced eneergy self-sufficiency in recent year in favour of economic efficiency. It was cheaper to buy refined products than to refine oil at home, so refineries were allowed to close. Australia still has two, but New Zealand has none at all. Australia also has viable coal mining, a coal to liquids plant, and gas, so it’s in a better position than New Zealand in some ways, but distances are also much larger and the climate more extreme and less forgiving.

This site tracks New Zealand’s energy situation for different fuel types:

NZ Fuel Reserve Monitor

Live NZ fuel reserve countdown with MBIE stock cover, vessel tracking, live fuel prices, and scenario analytics.

This energy crisis is being exploited, if not explicitly created, in order to force a rationing system for resource use. Already shippers are being told not to unload cargos in order to accentuate the crisis and increase the sense of fear and desperation. This exploitation of crisis is a reflection of limits to growth, which are both real and largely non-nogotiable, and the fear of elites as to the reaction eight billion people will have to the rsource pie shrinking substantially in a relatively short period of time. Humans tend to “fight like cats in a sack” during periods of contraction, and they blame their leaders, often very violently. In order to avoid this outcome, the fear-driven elites are attsmpting to construct an ironclad control grid to lock the population down and orevent any form of collective action. The control grid is also intended to act as a severely restrictive form of resource rationing, mediated through a financial system at the end if a debt cycle which is about to be converted into a digital gulag.

The covid era was a trial run for population compliance in a crisis, and the elites were pleased with the degree of compliance that their nonstop fear porn produced. They managed, by manipulation and harsh coercion, to get 5.6 billion people to poison themselves with a bioweapon. The mass poisoning has created excess deaths, chronic illness, many different disabilities, a wave of cancers (that is only just beginning), and reduced fertility. The spike protein pathology is likely now hereditary due to the ability of the pseudo-mRNA to transfect into the genome and the germ line. In addition, the covid era allowed the elites to force the closure of many small businesses (while allowing large corporations to steal their market share), to lock people into isolation for prolonged periods, to break up longterm relationships between friends and family, to create fear around associating with others, to reduce the elderly population in order to save on pension payouts, and to destroy trust, thereby tearing up the fabric of society. All of this would take years of peace to heal, but this is not an era of peace, and the energy crisis is about to exert an even greater degree of pressure. The attempt to use climate as z justification for extreme control measures appears to have failed, so energy crisis will now perform that function.

The goal of elites is extreme central control in every way they can possibly manage, combined with separating people as much as possible from the natural world. The energy crisis is going to morph into a food crisis due to unaffordable fuel and fertiliser, which also comes to us through the Straits of Hormuz. The central control answers are insect protein substitues from factories, lab-grown meat substitutes (starch and seed oil based and therefore highly inflammatory), indoor vertical farming, genetically engineered organisms (unlabelled), selective biocides, an emphasis on calories over actual nutrition (in order to undermine the heath of the population, reduce their capacity for collective action, and reduce their numbers over time), and a reformatting of soil biology with genetically engineered bacteria. All of these actions would be highly detrimental to the population while substantially enriching the Epstein class of oligarchs.

That oligarch class is international, and it’s coordinating the same actions in many countries all at the same time, with the same messaging, just as it did during the covid era. They’ve decided never to waste a good crisis, as it’s much easier to force through highly unpopular restructuring when people are afraid. The fear porn is intended to keep them that way. The Bank for International Settlements (BIS) in Geneva, and its wealthy owners (many of whom are Rothschild-connected, although other long-established banking families are also involved) is at the centre of this, and is acting through the World Economic Forum (WEF), which is now chaired by Larry Fink of BlackRock. BlackRock is the world’s largest asset management company, and will be becoming much larger as they force through tokenisation of assets in order to commandeer control of them on a single central ledger.

Healthy local communities are what the elites fear the most, which is why they’ve tried so hard to undermine and destroy them. Communities work together. They pool resources for the benefit of all. They share skills without the need for payment. They can construct time banks and local currencies to allieviate a liquidity crunch. They can come up with creative ideas quickly in response to crisis, as the occupiers at Parliament did during covid. They support each other physically and emotionally, in order to create resilience. This is exactly what we need to create today. Bring people together, build relationships of trust, and don’t fall prey to the fear porn pushing people into digital ID and then the digital gulag. There are many more of us than there are of them. We need to remember that.

Wars are about control over resources in order that those resources are available to act as collateral for loans. It’s not about mere access through the ability to purchase necessary resources, but about control to the point of ownership. Without that level of control, the trust required to back loans with those resources would not exist. This is why bankers such as Jamie Dimon are now weighing in on geopolitics, although bankers typically fail to understand the realities on the ground. A network of military bases, a sanctions regime, and threats backed up by old-school military force no longer suffices to intimidate in the modern era of missile and drone warfare, cyberattacks, and AI. Assymmetric warfare now heavily favours those who have moved with the times.

Shadow banking exploded to some $220trillion since the last financial crisis – because shadow banks (non-depository financial institutions) are unregulated, so they were able to carry on their ponzi schemes out of sight of the victims being fleeced. Nothing was learned after 2008. The same practices, and worse, continued, turning the global economy into a self-cannibalising zombie system consuming whatever stores of wealth the oligarchs behind the system could get their hands on. However, that process can only continue for so long before the shortage of collateral becomes obvious. The dire need to find additional resoucres tomuse as collateral isnthe driving force behind the wars in both Ukraine and Iran. In both cases, the aim is to balkanise the country in order to divide and rule, while stealing anything of value. BlackRock has already essentially bought Ukraine, and now insists that its investment be protected, as impossible as that’s turning out to be.

The US is now in a position where a third of its outstanding debt must be rolled over this year, since the treasury has been borrowing at the short end of the curve for years. Interest rates have since risen, so this debt would have to be rolled over at a substantially higher rate, which is unaffordable, as the interest burden on some $40 trillion of debt would skyrocket. The Trump regime has been attempting to force rates lower by pressuring the Federal Reserve, but this has not worked. Now the supply shock due to the war in the Gulf is going to set prices rising sharply, causing central bankers to raise rates instead of lowering them. Trump is reduced to attempting to calm the markets with claims of victory, but thismis not going to work. Narcissists think they can alter reality by sheer force of will, but reality is about to unfold anyway. That reality is going to involve the demise of the petrodollar, and with it the exorbitant privilege that goes with controlling the reserve currency. This will be a financial catastrophe.

Trump has threatened to bomb Iran “back to the stone age where they belong” if they don’t reopen the Straits of Hormuz, which they’re not going to do. This would, of course, be a major war crime, although no one seems to care about those anymore. This war is existential for Iran, and they intend to take any consequences in order to drive the US out of West Asia (ie the Middle East). The proposed plans would create such an obvious disaster that a number of generals refused to comply and have been fired. Several air raft have been lost in the last day, making it clear that Iran still has air defences. This increases the risk considerably.

With very little traffic transiting the Straits, Ansar Allah (ie the Houthis) planning to close the Bab-al-Mandab southern entrance to the Red Sea, and 40% of Russia’s export capacity offline for repairs due to Ukrainian strikes on oil infrastructure, the oil market will be extremely heavily impacted. However, not all consumers obtain their supplies through the affected areas. For instance, the US has domestic production, and Europe obtains supplies from Norway. Despite this, these consumers are also facing much higher prices due to price gouging, cartelised price fixing, crypto betting scams, and all manner of financial chicanery. Trump’s tweets are market manipulation for the benefit of his friends and family, who are making obscene amounts of money. Ordinary people are being squeezed from all sides while the ultra-wealthy Epstein class is benefitting enormously. They never let a good crisis go to waste.

Finance is the global operating system, and as such, those who sit at the top of the financial food chain can tweak geopolitics in many ways, in order to gain the outcomes they want through manipulation. Over time, as financialisation of everything in the west has taken off post the 1971 effective default in America (when Nixon closed the gold window), the ability of financial oligarchs to manipulate the system has increased enormously. So has the use of ponzi dynamics, meaning the introduction of destabilising positive feedback loops, even in critical subsystems of the economy where an approximation of stability is crucial. Finance subordinates sectors of the economy to the dynamics best suited for wealth extraction favouring the already wealthy.

Retail banks create fiat currency from thin air every time they make a loan, but they don’t create the interest they require for the loans to be repaid. The recipient must then invest in a productive asset or pass the debt on to someone else. People become collateralised debt obligations, and companies build equity in order to collateralise more borrowing. A debt-based ponzi scheme is born. The endgame is to dump the debt on the government in a taxpayer bailout.

Governments are no longer in charge. They’re simply the mangerial class, prostituting themselves to the various lobby groups, while needing to sell a narrative for their actions to the public, which still thinks voting makes a difference. Actual democracy was lost a long time ago. Now governments are the ultimate repository of debt, leading to asset stripping of the eventually bankrupt country. War typically follows, as cover for the necessary financial reset.

The transfer of hegemomic power follows a pattern, as I wrote many years ago. A centre rises, by extracting resources from its periphery and concentrating them at the new centre. Over time, the now rich centre outsources the actual work to its near periohery, while continuing to extract from its far periphery. The near periphery gains technology transfer, a work ethic, and a manufacturing base, while the centre becomes more decadent and lazy. Eventually, the centre collapses, a new centre arises in the former near periphery, and the pattern repeats, as I documented here, beginning arbitrarily with the Spanish empire and proceeding to the transfer from the US to China, as is now already underway:

Entropy and Empire – Applied Systems Thinking

In his recent book The Upside of Down, a review of which can be found here, Thomas Homer-Dixon interpreted the development of the Roman Empire in terms of thermodynamics. The success of the empire depended on its ability to extract energy surpluses, in the form of food, from the imperial territories and concentrate them at the centre,

America is the empire in decline, having allowed financialisation to hollow out its real economy, and financial oligarchs to rise to such a position of power that they now dictate all policy towards their own profit, and no longer even bother to hide their dominance over, and contempt for, the rest of the popualtion. They believe their power to be sufficient that they no longer need to care what the rest of us think. Their problem is the rest of the world. As empires fall, they typically enter Thucycidies Trap, where the hubris they experience from dominating their domestic population translates into a sense that the empire should be eternal and all-encompassing. In other words, it must suppress rising rivals, but the resulting conflict typically ends the over-extended empire instead.

The average interest on the $40 trillion of US is about 3.3%, but growth is expected to fall well short of that, and when the rate of growth is below the rate of interest on the debt, it becomes an exploding debt scenario. That leads to the unwinding of the debt cycle, which will result in an economic depression and major demand destruction. The Trump regime has been attempting to force the Fed to lower rates, so the debt could be rolled over at a rate below the rate of growth, but that has failed. Now that prices will inevitably rise due to the oil supply shock, and also the impact of shortages of other essential resources, interest rates will be raised rather than lowered. Rising prices are not inflation in and of themselves, but they’re the symptom of an increase in the money supply relative to available goods and services combined with a major collapse in available goods and services. The overall effect of the eventual debt collapse will be deflationary, as the majority of the money supply is credit, and the value of credit will collapse when the promises made can obviously no longer be kept. Demand destruction is deflationary.

in an attempt to stave off the crisis of severe undercollateralisation of existing debt, the Epstein class which runs the system will attempt to improve the collateral situation through converting illiquid assets to liquid through tokenisation, and also extracting and controlling all assets currently in the hands of ordinary people. This is the digital financial system they’re attempting to impose through the Bank for International Settlements (BIS) and the World Economic Forum (WEF), and it amounts to a slavery system, with total surveillance and control of all spending at the level of the individual. This requires digital ID as an entry point, which must be resisted by individuals who wish to remain independent. This will, however, be made very difficult, as the oligarchs will try to make digital ID a necessary condition for participation in society.

In the meantime, prices for essentials will rise, as will interest rates on outstanding debt held by companies and individuals, and also property and other taxes, as well as the cost if insurance. At the same time, unemplyment will be rising sharply, and wages for the still employed are likely to be cut. This is a perfect storm in financial terms, amounting to a financial seizure and a crash of the operating system. A major liquidity crunch is inevitable. The Greatest Depression is coming, and it will be far worse than the depression of the 1930s. Money from the Gulf countries via the petrodollar and private credit, the eurodollar market, and the Japanese carry trade are all under threat, and these are the factors that had been supporting the debt of the US empire. The destruction will encompass the IPO market (ChatGPT cannot IPO at high energy prices), the bond market, the private credit market, the fungible market for oil, the enegy market in general, and eventually the stock market.

The ongoing war will accelerate the collapse. The empire (a combination of the US, Israel, and western vassal states) has drastically underestimated the capabilities of its declared enemy.

The empire had thought a short war could crush Iran and allow it to commandeer Iran’s resources, but this has not happened. Iran had been preparing for this war for decades, with an enormous arsenal of drones and missiles, plus submarines, torpedos, and other unconventional weaponry, most of which is so far underground that it cannot be destroyed. It has no need of a conventional navy or airforce, so the elimination of those limited capacities has not diminished its ability to both defend and attack. Both the repressive Gulf monarchies and the apartheid state of Israel are in the process of being destroyed as a result. This could lead to the use of nuclear weapons by the empire, but even this is unlikely to take Iran down, as the military capacities would remain, and the population and economy are not highly concentrated. We’re likely looking at the rise of Persia as a major regional power.

The empire had been looking at profiting from rebuilding a ruined country, while also profiting from its stolen resources and using them as collateral for debt expansion, but that will not now be happening. Instead the world is fracturing into power blocks, with the empire set on its path to decline while energy-sovereign countries such as Iran and Russia do far better. In the US private ownership of resources means profits will continue to benefit only the few, while in countries with public ownership, the country as a whole can benefit. Existing global supply chains will be irrevocably broken, although regional ones will eventually re-emerge. Energy will continue to be scarce and expensive for the foreseeable future, and this will drastically alter the level of socioeconomic complextity that can be maintained. Ultimately, this means the digital gulag will fail, so an attempt at totalitarian control will likely give way to anarchy. The Build Back Better programme, which was intended to operate from the top down, will now need to be implemented from the bottom up, with considerable local variation to account for highly variable local circumstances. Building what cohension is possible at the local level, beginning right now, is the best way forward for those of us at the bottom of the financial food chain.

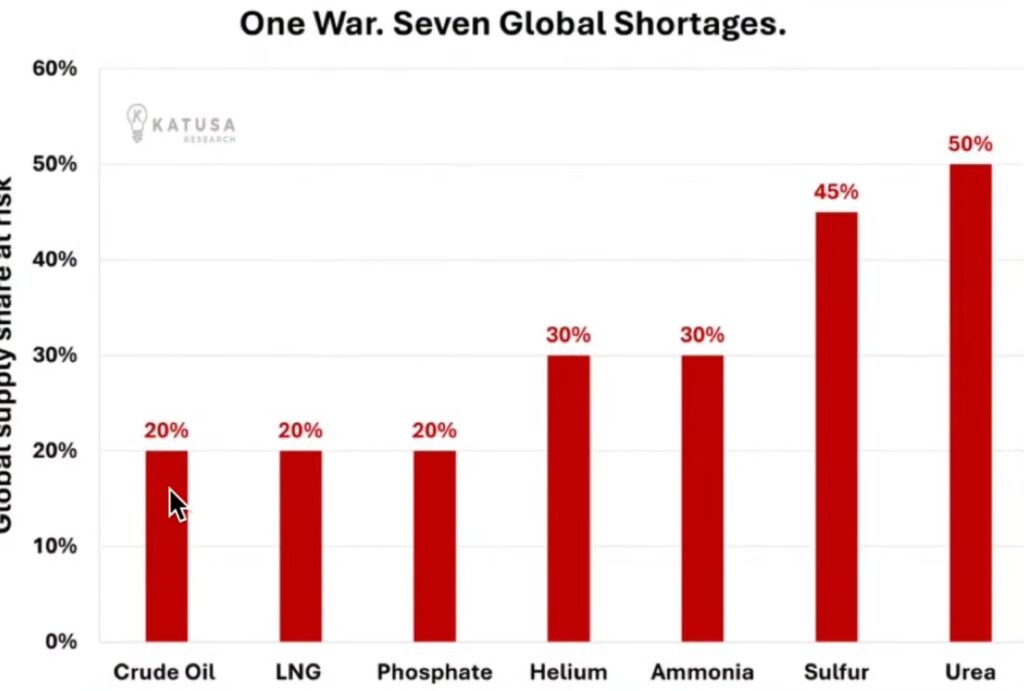

Neil McCoy-Ward covers many issues, primarily financial. Here he’s discussing critical resource shortages around the world as a result of the war, and the rationing systems being put in place. On a personal level, he’s been experiencing a ‘shoot the messenger’ effect, due to people’s fear of another lockdown, given how traumatic people found the covid era. Unfortunately another lockdown is very much on the cards, and it obviously doesn’t help to blame those who warned of this in advance. These are the global supply shares at risk:

The missing resources are all critical to various industries, and cannot be replaced. The global economy has been engineered for economic efficiency, meaning a global just-in-time system with highly integrated supply chains and very few stocks or reserves. This was the product of a high trust world (relatively speaking) at the top of a major financial cycle. That cycle is now ending, and trust is collapsing with economic contraction. All those interconnected supply chains are vulnerable, and many will fail. In the Great Depression of the 1930s, trade fell by 66% in two years, with trade wars, protectionism, neo-mercantilism, and gunboat diplomacy, followed by kinetic war. We’re looking at a similar breakdown today, but today we’re far more dependent on trade than we were then, and our newly brittle networks are vastly more complex. When a system such as ours goes into contraction, our economic efficiency turns into the straightest path to hell.

Countries are going to need to restore self-sufficiency, but how many citizens in many countries even know what their local reality would be in the absence of imports and exports? It’s going to be a steep learning curve, and it needs to be addressed as quickly as possible, beginning with working out where the essentials are going to come from. Anything non-essential can wait. Unfortunstely, the countries which benefitted disproportionately from globalisation can expect to suffer disproportionately from its demise, and this includes my own country of New Zealand, where we lie a long way from anywhere at the far end of supply chains.

“The closure of Hormuz has taken 34% of globally-traded crude oil, 12% of refined petroleum, 20% of LNG offline. It has taken 30% of urea and 25% of ammonia offline, putting the northern planting season at risk in the largest shock to food production in generations. Some 20% of aluminum production if offline too. In the chips supply chain, in addition to the LNG, 35% of helium, 60% of bromine, and 44% of sulphur are now offline.

Unless the war ends soon and Hormuz is reopened, this will be the single greatest stagflationary shock in the history of the modern world economy. And the costs are cumulative. The longer the war lasts, the greater the stagflationary shock and the more central banks must respond by monetary tightening.”

Professor Ted Postol is one of the foremost experts on nuclear technology and its effects. This is a very detailed, no-holds-barred presentation on what a nuclear strike on either Tehran or Tel Aviv would look like, and the the terrible effects it would have. The American regime has been comtemplating doing this, if not over a city then in an attempt to destroy Iran’s extensive underground infrastructure, some of which is 800m below ground. They appear to think that a nuclear war might be able to be contained, or might even be winable. This is not the case. There’s every reason to think this would escalate. Already, many states are considering building nuclear weapons, since it’s obvious that a nuclear deterrent is the only protection from abuse by imperial powers. The potential for the escalation ladder in any of several different conflicts, besides the existing ones, is enormous. The world has entered a war cycle, and those typically cost about a third of the population. This one could be much worse. Please listen to Professor Postol explain why.

This war of aggression, with the intent if not just regime change in iran but utter destruction of the country, is turning out to be an unmitigated disaster for the the US and Israel. They’ve entered a quagmire with no escape, and have repeatedly chosen to double down and escalate, but they have no clear goals, other than pure destruction, and no strategic vision, other than potentially to cripple China’s rise by curtailing its oil supply. Trump is flailing, knowing he’s caught in a trap and resorting to regular market manipulation in order to profit financially despite the disaster on the ground.

For Iran the situation is very different. While this is undoubtedly a crisis for them, as they’re losing many thousands of innocent citizens and important civilian infrastructure, it also represents an opportunity to reshape a great deal of the global economy in their favour. The US had controlled global oil flows and pricing for the decades since the 1974 advent of the petrodollar system, but that arrangement has now ended. America is being rapidly driven out of the Gulf entirely, with the loss of hundreds of billions of dollars in infrastructure – military bases, data centres, businesses, banks, universities etc. Iran is now in a position to take over that control in a seismic shift in global geopolitics.

Iran now controls the Straits of Hormuz completely. Ships need their permission to pass, and ships without that permission will be destroyed, as several already have been. Iran can mine the region at any time should they choose to do so. Already the shipping lane has been changed to lie much closer to the Iranian coast, so as to allow for visual inspection of shipping. Ships must prove that their cargos are contracted in yuan rather than dollars, and they must pay a toll determined by the Iranians. Ships have been paying two million dollars as a toll so far. Over time this will earn Iran enough to rebuild from the destruction of the war, so it amounts to involuntary reparations.

The flow of goods, not just oil, has now moved beyond the control of the US, and the situation is about to get worse for them since Ansar Allah (the Houthis in Yemen) are now planning to assist Iran by imposing conditions on passage through the Red Sea via the Bab-al-Mandab southern entrance. Control of volume and flow can confer pricing power, and undermine fatally dollar hegemony. The loss of dollar hegemony would be the equivalent of losing a major war, and in this case the US is likely to hit by both losing dollar hegemony and losing and majir war at the same time. The impact will be enormous. The petrodollar system generated the gargantuan money flows that allowed for the full financialisation of the US economy, at the expense of its real productive economy. Reversal of that trend, for an empire mired in forty trillion dollars of debt, evenbefore taking account of tens of trillions more in unfunded liabilities, will be catastrophic.

The situation is also catastrophic for Israel, which has drastically overreachedits potential in its zeal to create a Greater Israel encompassing most of the region. Their apparent belief was that the Iranian regime could be toppled easily, with no real price to pay. They underestimated Iran to an extent that is turning out to be tragic for them, as their citizens live in bunkers while the built environment takes terrible punishment. IDF generals are desperate. They’re running out of manpower and cannot recruit. They’re facing attacks from Ansar Allah in the south, a resurgent Hezbollah in the north, and both Iraq and Iran to the east. The country is small and indefensible now that the Iron Dome has essentially run out of interceptors. Moral is low and falling, although the blood lust remains and is increasing. The Knesset just passed a law allowing them to execute their Palestinian hostages, on trumped up charges in a court with over a 95% conviction rate. There are ten thousand such hostages, many of them children. They face hanging, often following years of horrendous abuse in Israeli jails.

War crimes and crimes against humanity are commonplace now, as international law, the laws of war and the Geneva Conventions have all been discarded in favour of the law of the jungle – might makes right. Unfortunately for those who consider themselves to be on the mighty side of the equation, they have over-estimsted their own capacity while drastically under-estimsting the capacity of their opponents. One of the latest terrible ideas has been attacking nuclear sites, which have always been off-limits before due to the potential for regional contamination.

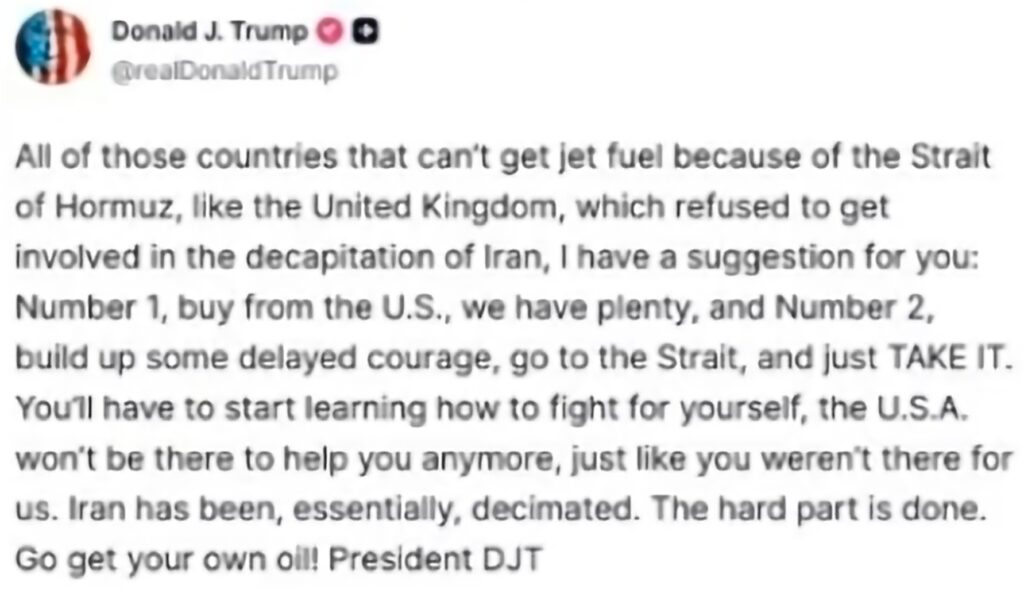

Most recently, Trump has indicated that he might simply give up and go home without achieving a single one of his many stated goals, which change regularly. Crucially, the Straits of Hormuz would remain under Iranian control unless others do something about it. Trump had attempted to corral vassals states into taking the obvious and overwhelming risk of doing so, but comprehensively failed. Trump’s response has been to sulk, and to promote buying American oil instead.

If the US does decide to abandon the war, it’s extremely likely that Trump and his Secretary of War Crimes, Pete Hegseth, will do as much damage as possible on the way out, in order to punish Iran for its ability to resist. They may even resort to the use of nuclear weapons, unless prewarned that doing so would bring other nuclear states into the conflict, which may have happened behind the scenes.

Air power never was the be all and end off of war, despite the biased views of the airforce. Destruction is possible, but not victory.

This extremely well qualified woman is passionate about the lives of her fellow service members. She knows they are about to be sacrificed as cannon fodder in a war conducted at the behest of another country – Israel. They cannot hope to win. Their inevitable deaths are intended to spur the American population into support for a war they currently oppose. The American regime doesn’t care. In his last term, Trump refered to military personnel as “suckers and losers”, according to his own chief of staff. He has no understanding of honour or sacrifice. Soldiers are just pawns to be sacrificed, and not even for any real purpose, because there’s no strategic vision for this war, and no plan. Serious military people who disagreed with Trump and his psychopathic Crusader of a ‘Secretary of War’ have been purged, leaving only hubris and delusion at the helm. The consequences for the entire world are likely to be catastrophic.

The people of the Gulf live in a desert, but the population of the region far exceeds the natural carrying capacity. This has been possible due to the huge oil wealth of the area that’s allowed the various monarchies to build desalination plants to provide for adequate water supplies. They’ve also been building complex modern cities, along with ridiculous infrastructure like palm-shaped islands and indoor ski hills, allowing the population to live in an elevated state of luxury, with imported servants from all over the world, also sustained by the desalination plants. Now all that infrastructure is under threat, and the authoritatian monarchies are beginning to experience a rapid convergence with reality.

The Gulf countries are all vassals of the US empire, hosting huge American military bases, many luxury-loving western expats, data centres, American universities and more. Under the petrodollar system, they’ve invested heavily in American weaponry, not so much for anticipated use, but as tithe to the American military industrial complex. Now the region is at war – war begun by the US at the behest of Israel. The US is using the military infrastructure it built to conduct the war, but this is implicating the Gulf monarchies in the conflict, making them targets for retaliation. Some are more willing than others, and at least one – Qatar – has already said enough is enough, after their new $26 billion LNG plant took $20 billion of damage and will be offline for up to five years.

Israel, which has long coveted the land of the Arabs for lenbensraum, has a vested interest in keeping the conflict going, and specifically in encouraging Iran to retaliate against Gulf infrastructure. If the US appear reluctant to strike, Israel takes matters into its own hands in targeting Iranian infrastructure on a false flag basis. The intention is to provoke an internecine conflict between the Sunni monarchies and Shia Iran, in order to watch them destroy each other for Israel’s benefit.

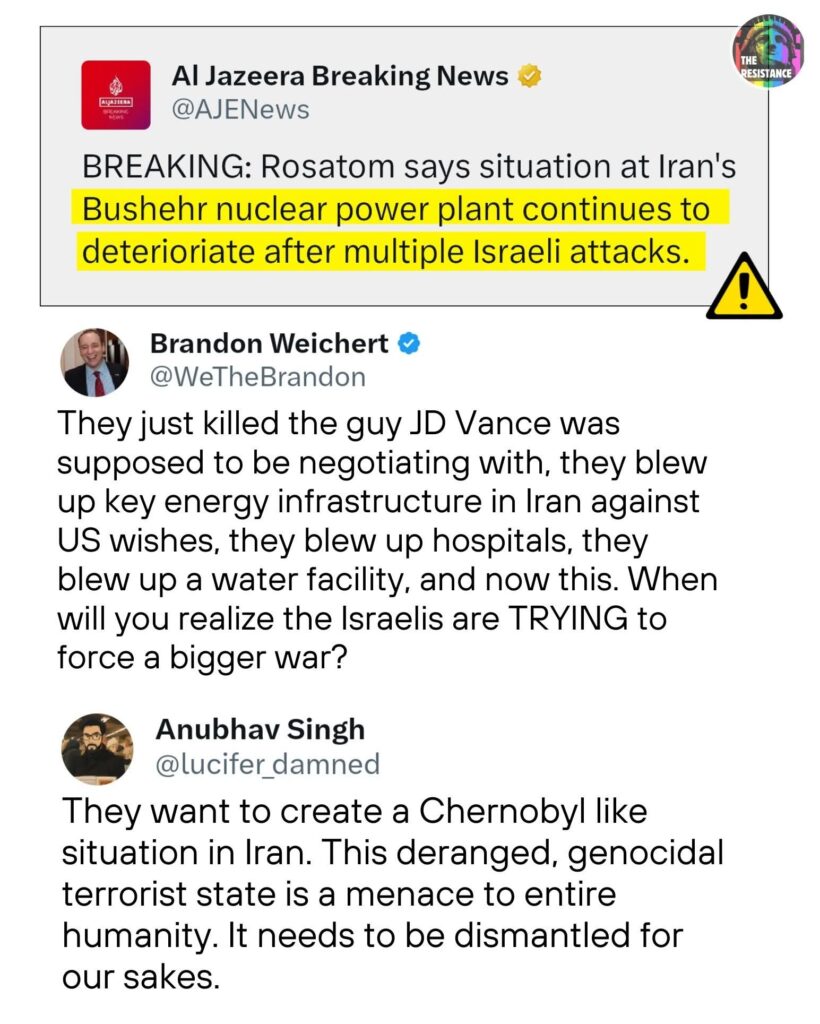

Trump, who is likely being blackmailed as well as bribed to follow Israel’s lead, has been threatening to destroy Iran’s civilian infrastructure, notably its power grid, if a deal to open the Straits of Hormuz is not reached, but he’s building in progressive delays. Israel has stepped into the breach and begun to do what Trump threatened, including bombing Iran nuclear reactor at Bushehr multiple times. Iran is retaliating as promised, against both Israel and the Gulf countries, but so far in a measured way. The critical factor will be the desalination plants, upon which the Gulf is utterly dependent. Iran itself only uses desalination as a minor supplement to its water supply, but some Gulf countries are virtually 100% dependent on it, and all obtain the clear majority of their water in this way.

If the desalination plants are taken out, the result will be catastrophic. There is no alternative source that can be called upon for the millions of people living in the region. A lack of water in a desert is a death sentence in a matter of days, and it would be impossible to evacuate the region before a humanitarian catastrophe set in. The wealthy are already leaving the region if they can, although they mostly can’t expect any help from their own governments, and airports are being damaged. Others are simply trapped, hoping that their water supply survives. The depopulation of the Gulf is a distinct possibility at this point, but it isn’t Iran’s doomsday plan, it’s Israel’s.

The aggressors are not faring well in this war, even though they conceal or deny the damage they’re taking, and the consequences for the rest of the world are escalating. The energy supply impacts are bad enough – 20% of the world’s oil production offline – and states of emergency being declared in Asia. Other impacts may have a less immediate impact, but not less important to the global economyand the global population. 35% of the world’s fertiliser comes through the Straits of Hormuz, along with the sulphuric acid needed for chemical extraction in many industries, the helium required for the manufacture of computer chips in Taiwan, and many other commodities.

The cost and/or lack of availability of fertiliser is hitting the northern hemisphere exactly at planting time, guaranteeing that the window for planting will pass with much less planting done. Yields are very likely to be well down this year. The cost of agricultural fuel is also hitting farms very hard. In the southern hemisphere, expensive fuel and the looming potential for rationing, are affecting harvest season. This will all get much worse before it gets better, even if the war were to somehow end tomorrow, which is extremely unlikely.

Iran will be setting the timetable for the conflict, because they have escalation dominance. They have set conditions for the end of the war that the US will be unwilling to meet, so hostilities will continue. Declaring a false victory and going home will not be an option for America this time. Trump is trapped, and will take the blame for all of it when it turns into a complete disaster, which it will. Those who talked him into it, or blackmailed him into it, may escape accountability unfortunately.

Iran has 270 degree fire control over the Straits of Hormuz. They still have air defence, and many sea defences, despite lacking a conventional airforce or navy. They have huge numbers of the drones that have been so pivotal in the Ukraine war, and yet to use their most modern missiles. They have home field advantage over very challenging terrain. They are very unlikely to lose, even if carpet bombed with nuclear weapons. It’s very difficult to defeat a people who prize martyrdom and refuse to run even when their street gatherings are bombed.

In the meantime, the Straits of Hormuz now operate a tollgate system, requiring visual inspection to weed out vessels from hostile countries, a substantial toll paid in yuan, and evidence that the cargo has been purchased in yuan. This will generate billions of dollars per year for the Iranian economy, and will hasten the establishment of the petroyuan and the demise of the petrodollar.

Israel cleaerly wants the complete destruction of Iran as a state, so any attempt at an off-ramp is likely to be undermined by false flag attacks. Israel is already attacking infrastructure in the Gulf states with a view to starting a civil war between the Sunni and the Shia, so that they might destroy each other. Israel isn’t interested in regime change in Iran because that wouldn’t go far enough. They want the country bombed into the stone age, and balkanised into ethnic regions. Persians are just over 60% of the population, which also includes Kurds, Azeris, Baluchis, Arabs, Zoroastrians, Bahais, Jews, and Christians, all of whom have lived together for centuries. Some may prefer independence, but most do not. Israel will try to divide and rule as best it can.

It’s profoundly sad that Jews around the world who have nothing to do with this, and generally oppose it vehemently, will nevertheless face a major backlash for the actions of the fascistic zionists, a majority of whom are not even Jewish. That majority are imperial colonialists of European descent. All the hysteria about anti-semitism now is manufactured, but in the future it will almost certainly be real.

Trump gave Iran 48 hours to open the Straits of Hormuz, then extended it by five days (to allow for ground forces to arrive in the region), then extended it an extra ten, but Israel took matters into its own hands and bombed Iran’s steel plants. Iran has already said that bombing such infrastructure would be met with the destruction of energy and desalination infrastructure across the Gulf. This is exactly what Israel wants. The war must comtinue, and the various Muslim states must be encouraged to destroy each other. So far Iran has not engaged in mass retaliation. Their responses have always been measured so far, with responses in kind, but not escalation. It remains to be seen if the Israeli attacks continue to provoke regional destruction, and if America can withstand the carnage that’s likely to occur as a result of boots on the ground. At some point, the US may be forced to abandon Israel and the region, at which point Israel may cease to exist. Both aggressor countries appear to have bitten off more than they can chew.