Join Nicole and Alia for Episode 2 which is all about Energy Limits. Remember you can pick up a free nifty cheat-sheet for the session by registering on the Ready, Set, Prep page: https://www.voicesforfreedom.co.nz/ready-set-prep

Jeff Rubin and Oil Prices Revisited

Jeff Rubin, former chief economist with Canadian bank CIBC, is very well known for his predictions of exponentially increasing oil prices (see for instance this 2009 lecture). Mr Rubin’s position was that prices would continue their rise due to a confluence of circumstances – that conventional supplies have peaked, that unconventional sources are expensive to produce and that demand would continue to grow with the energy requirement inherent in expanding global trade.

According to Mr Rubin, the assumption that transport costs would remain marginal led to the 2008 oil price spike, causing a global recession. In his opinion, high oil prices, not the sub-prime mortgage crisis, were the primary driver of financial crisis. This opinion is shared by many commentators. The simplistic approach of prediction by trend extrapolation is similarly common. In contrast, anticipation of trend changes is rare. Continue reading “Jeff Rubin and Oil Prices Revisited”

Peak Oil: A Dialogue with George Monbiot

George Monbiot recently made a major about-face on his peak oil stance, on the grounds that unconventional oil represents a new reality. The basis of his u-turn is a recent report on unconventional oil by Leonardo Maugeri, (former) oil executive at Italy’s Eni, published at Harvard University, where Maugeri’s a Senior Fellow at the John Kennedy School, Belfer Center, which we discussed here at TAE in Unconventional Oil is NOT a Game Changer. Continue reading “Peak Oil: A Dialogue with George Monbiot”

Unconventional Oil is NOT a Game Changer

National Photo Co. Fossil Fuel 1920

Washington, D.C. “Penn Oil and truck.”

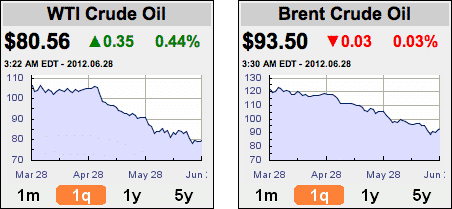

Oil prices have been falling.

This is no surprise to us here at The Automatic Earth, as our position is that the 2008 price peak will stand for a very long time, and that the rise from the 2009 low has been a counter-trend rally. Prices of many assets have been moving with the ebb and flow of confidence, and therefore of liquidity, in this era of extreme financialisation, and commodities are no exception.

As we have pointed out many times, prices do not reflect the fundamentals of supply and demand in any particular industry. If they did so, equities and different commodities would not move in relative sychrony, yet they have often done so.

Instead, prices reflect a combination of general confidence (or lack thereof) and the perception of future scarcity or glut, whether or not that perception is, in fact, accurate. Commodities top on fear of shortages. When there is a perception of scarcity, speculators bid up the price in advance of what the fundamentals would justify at that time, as they did in the run up to the 2008 price peak.

When the speculative bubble bursts, the sector is dumped and the price collapses as speculation goes into reverse. In 2008, commodities in general fell 58%, and oil prices plunged 78% in five months as the financial crisis sucked liquidity out of the system and the perception of imminent scarcity disappeared.

With the temporary resurgence of confidence from the 2009 bottom, liquidity returned, and, increasingly, so did the perception of scarcity for commodities in general and for oil specifically. Prices were bid up again, although not to the previous high, even though analysts extrapolating the trend forward were calling for a much larger commodity price spike than 2008.

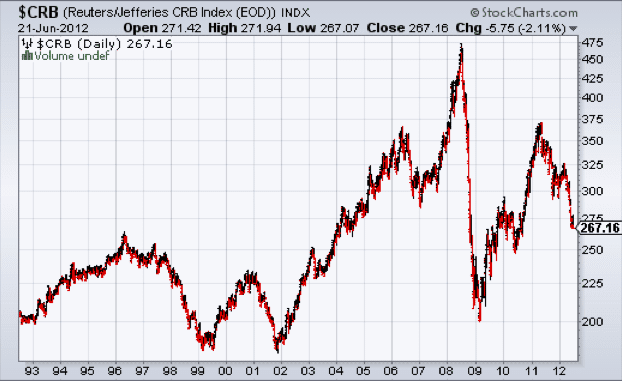

Commodity prices in general peaked in May 2011 and continue their retreat.

Confidence is ebbing as the scope of the financial crisis centred in Europe becomes increasingly evident, and vulnerabilities in other regions and sectors of the economy emerge. Even the Chinese juggernaut (the primary driver of commodity demand) is visibly faltering.

Retreating liquidity and persistent economic weakness act to undermine commodity prices further. This process is far closer to its beginning than its end. As the global credit bubble of the last thirty years implodes, we will be heading right in to the teeth of liquidity crunch, economic seizure and another deflationary Great Depression. Under such circumstances, we can expect demand to be weak for many years, and with falling demand will come falling price support.

At the same time, in the case of oil, we are seeing a sharp reversal of perception – from one of scarcity to one of glut – as pundits discuss how technological innovations, including horizontal drilling and hydraulic fracturing, will increase global supply dramatically. De-conventionalisation of oil supply is touted as the solution to peak oil for the foreseeable future.

Euphoria particularly surrounds the projections for US production, with talk of the country becoming both energy independent and an exporting powerhouse – a New Middle East.

Leonardo Maugeri:

Thanks to the technological revolution brought about by the combined use of horizontal drilling and hydraulic fracturing, the U.S. is now exploiting its huge and virtually untouched shale and tight oil fields, whose production although still in its infancy is already skyrocketing in North Dakota and Texas.

The U.S. shale/tight oil could be a paradigm-shifter for the oil world, because it could alter its features by allowing not only for the development of the worlds still virgin shale/tight oil formations, but also for recovering more oil from conventional, established oilfields whose average recovery rate is currently no higher than 35 percent.

The natural endowment of the initial American shale play, Bakken/Three Forks (a tight oil formation) in North Dakota and Montana, could become a big Persian Gulf producing country within the United States. But the country has more than twenty big shale oil formations, especially the Eagle Ford Shale, where the recent boom is revealing a hydrocarbon endowment comparable to that of the Bakken Shale. Most of U.S. shale and tight oil are profitable at a price of oil (WTI) ranging from $50 to $65 per barrel, thus making them sufficiently resilient to a significant downturn of oil prices.

World oil production capacity to 2020 (Crude oil and NGLs, excluding biofuels)

From: Maugeri, Leonardo. “Oil: The Next Revolution” Discussion Paper 2012-10, Belfer Center for Science and International Affairs, Harvard Kennedy School, June 2012.

The difficulty is that an analogous scenario has unfolded before, in the natural gas industry. Out of sync with other commodities, the boom and bust in natural gas is giving us a glimpse of the future for unconventional oil. The extraction techniques are the same ones that have generated tremendous hype, while simultaneously setting up a ponzi scheme in flipping land leases, creating the perception of supply glut, crashing the price of natural gas in North America to far below break-even, amplifying financial risk for increasingly indebted producers, and threatening to put those same producers out of business.

This is the dynamic that is set to lead North America into a natural gas supply crunch over the next few years, as we discussed recently in Shale Gas Reality Begins to Dawn.Those involved in unconventional oil would do well to take note.

The drilling costs are high, as are the decline rates (“While some have been able to yield as much as 1,000 barrels a day, the rate then falls off to 65 percent the first year, 35 percent the second, and 15 percent the third”), and the EROEI is very low in comparison with conventional oil. As with unconventional gas, which suffers from the same obstacles, the industry is set on an accelerating drilling treadmill in an attempt to grow equity by expanding the reserve base with the cash flow generated.

Continued expansion is necessary to maintain the perception of company value. In other words, the industry is based on ponzi dynamics. So long as prices hold up, we can expect it to continue, but if we look at the broader economic context in conjunction with the lessons derived from unconventional gas, there is every reason to expect that the production boom is temporary, precisely because these circumstances will generate a price collapse.

Estimates of the price required for the new supplies to be economic vary. The consensus appears to be that there is a sufficient price cushion to withstand a fall, but producers are not anticipating a major one. Unfortunately for them, we can expect the perception of glut, combined with deepening economic depression, to force prices down to the cost of the lowest price producer, and quite possibly lower, at least temporarily. Companies on the unforgiving drilling treadmill will be facing increasing financial risk, and over the next few years, as over-extended and over-indebted companies go out of business, we can expect a supply crunch to develop.

The timescale is difficult to predict, as there are many factors with different timeframes to consider. Large scale deleveraging, which is set to unfold over the next few years, will have a tremendous impact on project capital availability, on demand, and on the affordability of operating and maintaining existing infrastructure. It will also be very difficult to build out new oil transport infrastructure to cope with changing energy supply patterns. The infrastructure mismatch will put continued downward price pressure on North American oil in comparison with international supplies, reducing the fungibility of oil.

Marin Katusa:

Oil Price Differentials: Caught Between Sands And Pipelines

North America has a long history of oil production and processing. Decades of producing oil and consuming lots of petroleum products have left the continent with a pretty good system of pipelines and refineries but pipelines are annoyingly stagnant things that tend to stay where you build them. And it turns out that the pipelines of yesterday are in the wrong places to serve the oil fields and refineries of today.

America’s oil infrastructure was built around two inputs some domestic production and large volumes of imports. You see, while the Middle East may be the biggest producer of crude oil in the world, most of the refining occurs in the United States, Europe, and Asia. There are two reasons for this. The first is that it’s easier to ship massive volumes of one product (crude oil) than smaller volumes of multiple products (gasoline, diesel, jet fuel, and so on). The second reason is that refineries are generally built within the regions they serve, so that each facility can be tailored to produce the right kinds and amounts of petroleum products for its customers…

…Remember how the US’s oil pipelines were designed primarily to move refined products from the Gulf region and the coastal refineries to inland customers? Well, those pipelines of yesterday now run the wrong way.

The production boom in shale oil has momentum, and that is likely to carry on for some time, even in the face of sharply falling prices, as has been the case for natural gas. The rig count in shale oil production is skyrocketing, even as the rig count for natural gas falls, and production lags rig count.

The quantity of recoverable oil has been considerably hyped, and this resource is not going to represent a game-changer. In fact it would not even if we were not facing economic circumstances set to crash production.

Robert Rapier:

Does the U.S. Really Have More Oil than Saudi Arabia?

The estimated amount of oil in place (the resource) varies widely, with some suggesting that there could be 400 billion barrels of oil in the Bakken. Because of advances in fracking technology, some of the resource has now been classified as reserves (the amount that can be technically and economically produced). However, the reserve is a very low fraction of the resource at 2 to 4 billion barrels (although some industry estimates put the recoverable amount as high as 20 billion barrels or so). For reference, the U.S. consumes a billion barrels of oil in about 52 days, and the world consumes a billion barrels in about 11 days.

In addition, the enormous number of expensive wells required would takes decades to drill with the rigs available, even if considerable efforts were made to increase their number, meaning that the oil that is there would be produced very slowly.

Beyond the shale oil of the Bakken in North Dakota or the Eagle Ford in Texas, there are other forms of unconventional oil that form part of the North American production boom hype.

Robert Rapier again:

When some people speak of hundreds of billions or trillions of barrels of U.S. oil, they are most likely talking about the oil shale in the Green River Formation in Colorado, Utah, and Wyoming. Since the shale in North Dakota and Texas is producing oil, some have assumed that the Green River Formation and its roughly 2 trillion barrels of oil resources will be developed next because they think it is a similar type of resource. But it is not.

The prospects for some of these are significantly worse than for shale oil, especially where the EROEI is even lower. Colorados oil shale in particular is unlikely ever to amount to much. While shale oil is a liquid hydrocarbon trapped in low permeability source rock, which can be liberated through fracking, oil shale is not a liquid at all, but solid kerogen that requires tremendous energy inputs to be separated from the source rock. Those required energy inputs mean a rock-bottom EROEI. Costs in monetary terms are sky-high as well.

Elliott Gue:

The Difference Between Oil Shale and Shale Oil

To generate liquid oil synthetically from oil shale, the kerogen-rich rock is heated to as high as 950 degrees Fahrenheit (500 degrees Celsius) in the absence of oxygen, a process known as retorting.

There are several competing technologies for producing oil shale. Exxon Mobil has developed a process for creating underground fractures in oil shale, filling these cracks with a material that conducts electricity, and then passing currents through the shale to gradually convert the kerogen into producible oil. Royal Dutch Shell Plc buries electric heaters underground to heat the oil shale.

Although estimates of the cost to produce oil shale vary widely, the process is more expensive and energy-intensive than extracting crude from Canada’s oil sands. Producers would require oil prices of roughly $100 a barrel before this capital-intensive process would be feasible on a commercial scale.

Shale oil may have an EROEI of approximately 4, while tar sands would come in at 3 and oil shale would be 2 or less.

Cutler J. Cleveland and Peter O’Connor – A comparison of estimates of the energy return on investment (EROI) at the wellhead for conventional crude oil, or for crude product prior to refining for oil shale

Humans are prone to grasp at straws and believe in fantasies rather than face unpleasant realities. Believing that unconventional fossil fuels can maintain business as usual is a fantasy. We cannot run our current complex society on low EROEI energy sources.

We are still facing peak oil, and, on the downslope of Hubberts Curve, we will be running faster and faster on our accelerating treadmill just to slow the decline in supply. Unconventional supplies with lower and lower EROEI are not going to change that picture, and the crash of prices that will happen thanks to economic depression will aggravate the situation considerably in the short term. We can expect prices to fall faster than the cost of production, and many corporate casualties to emerge as boom turns to bust, as it always does.

The next few years will be remembered for financial crisis, where it will be money in short supply rather than energy. As economic contraction proceeds, and purchasing power falls substantially due to the collapse of the money supply, demand for energy will – temporarily – fall a long way. Beyond that, as the deleverging comes to an end and the economy begins to stabilize somewhat (probably between five and ten years down the line), we are likely to see a supply crunch develop.

With that we are likely to see a major price spike, and the potential for resource wars will grow dramatically. Oil is liquid hegemonic power, and conflict can be expected to develop when it is perceived to be scarce. Thats not where we find ourselves today, but it is where the future is taking us.

Get Ready for the North American Gas Shock

In this era of global bubble-blowing we have seen speculative fever flourish in relation to many different asset classes. At the peak of a bubble the euphoria can be palpable, and the perception that ‘it’s different this time’ confers a sense of invulnerability that justifies throwing caution to the wind.

Speculators cease to worry about how much they pay for an asset, since they think someone else will always pay more later. Unfortunately for those caught up in powerful swings of herding behaviour, it’s never different this time. Boom inevitably turns into bust, because the supply of Greater Fools is not infinite after all.

Speculative financial flows seeking ‘alpha’ can overwhelm important sectors of the real economy. Price, driven by perception rather than by reality, significantly over-reaches the fundamentals. Demand is artificially brought forward. That apparent demand drives considerable mal-investment and a pathological level of risk-taking. When the bubble reaches its maximum extent and implodes, speculation moves into reverse and the sector is dumped.

The artificial demand stimulation disappears, leaving a demand vacuum. The scale of the mal-investment becomes obvious, and prices head for a significant undershoot of the fundamentals. A bubble that created virtual wealth temporarily, leaves very real economic wreckage in its wake. When a critical economic sector is affected, the fallout can be very painful. Continue reading “Get Ready for the North American Gas Shock”

Oil, Credit and the Velocity of Money Revisited

Let me try to resolve apparent contradictions by answering some questions from a TAE reader:

Q: In 1933 there was a shortage of everything. Commerce had been dead for enough years – killed by gold- buggery – that there was shortages except for crops that were rotting in the fields (and petroleum that was wasted, according to Jeffrey Brown, who I believe.) No money meant no production = shortages = no commerce = no new money in the system in a self- reinforcing cycle. Citizens hoarded paper dollars as they had hoarded specie. Paper dollars were still worth more than (pauperish) 1930’s commerce.

Continue reading “Oil, Credit and the Velocity of Money Revisited”

Energy, Finance and Hegemonic Power

The interface between finance and energy will prove to be the most important determinant of the way the Greater Depression we are rapidly moving toward will play out in practice. For those here who may be unaware of peak oil, the point is that global oil production appears to have reached a production peak that it will not be physically possible to exceed. Oil discoveries peaked decades ago and we have since been increasing production from large existing fields using ever more complicated and expensive technology, in order to supply increasing global demand from decreasing reserves.

The production peak does not mean that oil is imminently running out – in fact there is probably half of all the oil that ever existed still in the ground, but it is the expensive and relatively inaccessible half. We can no longer increase production and production will fall over time as we continue to use up reserves which are not being replaced by new discoveries. Although discoveries continue to be made, they are few and far between, and of much smaller size than the giant fields we have relied on for so long. As they are much more challenging to produce, they rely on high oil prices in order to remain commercially viable. Continue reading “Energy, Finance and Hegemonic Power”

A Mackenzie Valley Pipe-Dream?

A gas pipeline along the Mackenzie Valley has been discussed on and off for over thirty years, since gas was initially discovered in the area of the Mackenzie delta. However, the project has long been a bone of contention between the companies seeking to develop and sell gas reserves, environmentalists and First Nations people living in the regions through which the pipeline would pass. While gas supplies were plentiful, and prices therefore low, the companies were content to sit on the reserves, but renewed interest developed in recent years as natural gas prices increased against a backdrop of low interest rates and an investment boom in the gas-hungry tar sands.

Click to Enlarge

Click to Enlarge

Click to Enlarge

Although gas prices have since fallen and interest rates have risen, there remains an understanding that the gas market is destined to become progressively tighter in the future as existing gas supplies dwindle in the face of strong demand on both sides of the border. Interest in building a pipeline to bring Mackenzie gas south remains strong, although construction cost estimates have increased substantially, even over the last couple of years. As the federal government gets closer to reaching agreements with the First Nations involved, the last hurdle to construction may soon fall. For First Nations communities, however, the deal may just tie them even more tightly to an unsustainable fossil fuel dependency at the peak of the petroleum age.

The History of the Pipeline – the Berger Commission

The Mackenzie River – or Deh Cho, meaning Big River – flows 1,730 kilometers north from Great Slave Lake in the North West Territories to Arctic Ocean, where it forms an extensive delta. The river, an important transportation route to the western arctic, is a lifeline for several different cultural groups. The Dene are an aboriginal nation living along the river valley, the Inuvialuit – descended from Inuit and European parents – reside along the mainland Arctic coast, the Inuit primarily populate the arctic islands, the Metis are of mixed First Nations and European heritage, and there are also populations of non-native Canadians. The population density is very low.

A Mackenzie Valley pipeline was first proposed in the 1970s, after the discovery of gas fields in the Mackenzie delta. At the time it was billed as the biggest project in the history of free enterprise. A federal royal commission, under Thomas Berger, was appointed in 1974 to consider the proposal and their socio-economic impact on the North. The timing of the inquiry coincided with an era of native activism instigated by the government’s 1969 proposal to abolish treaty rights and native reserves, withdrawn after a storm of protest. The commission held hearing across the north in 1975/76 and in 1977 issued a report recommending the pipeline project be delayed at least ten years – until native land claims could be settled. Berger warned that the infrastructure supporting a northern energy corridor would be enormous and the impact on the inhabitants of the region and its environment would be very significant.

At the time, native leaders were staunchly opposed to the pipeline. For instance, Chief Frank T’Seleie accused oil company executives at the Berger commission hearings of planning to destroy a people with 30,000 years of history for the sake of a twenty year supply of gas. Thirty years later, T’Seleie and Stephen Kakfwi, another vehement former pipeline opponent subsequently elected Premier of the Northwest Territories, are strong backers of a Mackenzie Valley pipeline. The difference in stance is a reflection of a newfound capitalist spirit amongst many aboriginal leaders and their people. They originally saw the pipeline as an attempt by southern business interests to exploit the resource wealth of the north with little regard for the inhabitants. Now, however, they are included in the development process, where they have the opportunity to invest directly in pipelines and other associated businesses and to earn resource revenue.

Gas in the Arctic – the Three Anchor Fields

Canada’s north is estimated by the National Energy Board to contain some 153 tcf of natural gas, or one third of Canada’s remaining natural gas reserves. An estimated 64 tcf of these reserves, only 9 tcf of which has actually been discovered, lie in the Beaufort-Delta area that would be served by the Mackenzie Valley pipeline, although significant additional reserves are expected to be discovered along the pipeline route to the south of the Delta. The arctic islands of Nunavut are thought to contain 63 tcf, but an almost total lack of infrastructure may prevent those reserves from being developed.

Click to Enlarge

The three anchor fields for the Mackenzie Gas Project, all of which were discovered in the early 1970s, are Parsons Lake, Taglu and Niglintgak. Parsons Lake, estimated to contain 1.8 tcf of natural gas, is jointly owned (75%:25%) by ConocoPhillips and ExxonMobil, while Taglu, estimated to contain 3 tcf, is owned by Imperial and Niglintgak, estimated to contain 1 tcf, is owned by Shell. If the pipeline goes ahead, the four companies are expected to invest at least $2.2 billion developing these fields.

The initial amount of gas expected to be shipped from the three anchor fields along a Mackenzie Valley pipeline is approximately 0.8 bcf per day, but pipeline proponents expect this to increase significantly due to additional exploration and development in the area once a pipeline is actually built. The companies planning to construct the pipeline expect it to carry 1.2 bcf per day once additional production comes on stream. Without the pipeline, production in the Northwest territories seems set to continue declining. According to the department of Indian and Northern Affairs, production fell 68% between 2001-2005.

The Mackenzie Gas Project

The Mackenzie Gas Project is gargantuan in scale. Imperial Oil, which is to construct the pipeline if it is approved, has yet to release a new cost estimate, but it has been suggested that the cost could reach $10 billion. The project consists of five parts: three natural gas field production facilities, a gathering pipeline system, a gas processing facility near Inuvik, a natural gas liquids pipeline from the Inuvik area facility to Norman Wells and a natural gas pipeline from the Inuvik area facility to northwestern Alberta. The pipelines are to be constructed underground along most of the length of the Mackenzie River tunnelling under 500 rivers and streams. The main pipeline would cross four aboriginal regions in the Northwest Territories – the Inuvialuit Settlement Region, the Gwich’in Settlement Area, the Sahtu Settlement Area and the Deh Cho Territory. A short segment would be built in northwestern Alberta near the border with the Northwest Territories, where it could impact on Dene Tha land.

Click to Enlarge

Environmental Concerns

The Mackenzie Valley watershed covers almost a fifth of Canada – an area twice the size of Ontario. It is the largest in Canada and its northern reaches are virtually pristine. Environmentalists are extremely concerned about the impact a pipeline would have on the region. They point to fragmentation of wilderness, loss of biodiversity, increased greenhouse gas emissions, reduction of boreal carbon sequestration capacity, exposure of wildlife to hunters or predators and the potential for permafrost melting.

Although the temperature of the natural gas in the pipeline is to be controlled in order to minimise temperature effects on the permafrost and on the pipeline itself, the potential would still exist for pipeline damage due to frost heaving. This could lead to leaks of natural gas or natural gas liquids, which could case environmental damage and potentially explosions or fires. Given that the effects of climate change are expected to be more severe in the north than in other regions of Canada, the pipeline could end up embedded in watery soil rather than frozen ground.

Although 120-foot-wide right-of-way would be constructed during winter in order to minimise permafrost damage due to heavy equipment, the construction phase would still have very significant impacts on the environment. Construction staging areas, barge landings and camps for thousands of workers would be required, necessitating clear areas of clear-cutting. Increased sedimentation in the river could harm fish habitat.

Once a pipeline has been built, environmentalists are also concerned about the impact an increased level of exploration and development activity would have on the fragile environment of Northwest Territories.

The Current Review Process

The current review process is divided into two parts. The National Energy Board (NEB) has been examining the engineering design and economic feasibility of the project since early 2006, while the Joint Review Panel (JRP) has been conducting hearings into the environmental and social consequences of the project. The project requires support from the JRP and subsequent regulatory approval from the NEB. Imperial Oil, which would build the pipeline, would then make its decision as to whether or not to proceed based on economic factors.

The Joint Review Panel has extended its series of public meetings until April 2007, although the process may be complicated by a recent court ruling which could require the consultation process to be restarted. The court found that the Federal government had failed to consult with the Dene Tha First Nation of northern Alberta as to the impact of the pipeline on its territory near the terminus of the proposed pipeline. The judge ruled that the JRP could not file its report until another hearing made recommendations as to remedies for the 2,500 Dene Tha.

Pipeline Construction – Increased Costs and the Quest for Government Subsidies

The most recent cost estimate for the pipeline put the price at $7.5 billion in 2003 dollars. Although it has not yet released a new cost estimate, Imperial Oil has said there have since been significant upward cost pressures, particularly on labour and steel, which could have raised the cost to over $10 billion. In addition, natural gas prices recently fell from $12 per million btu to below $5 per million btu. Imperial has said it is concerned about the economics of the project under the present circumstances and has said it is seeking fiscal certainty from the Federal government in order to be confident about its expectations.

Imperial’s cost review, which was to have concluded by the end of 2006, will extend well into 2007. The company had been seeking $1.2 billion in federal tax benefits and other assistance when the project had been expected to cost $7.5 billion, but now federal officials are expecting a request in the $2 billion range. The government is, however, apparently reluctant to provide a major subsidy to Imperial given the profitability of major oil companies. With several provinces making requests of their own federal money to support energy projects, the government seems unlikely to add to the funds it has already set aside. These funds include $500 million to address socio-economic impacts on indigenous communities due to the planning and construction of the pipeline, $75 million to increase its own capacity to review the Mackenzie Gas Project and $21 million for the economic development of the Deh Cho First Nations and for their participation in the project review. However, in September a government representative said it would be willing to consider an equity stake in lieu of subsidies.

Alternatives North, a social alliance of churches, labour unions and environmental groups based in Yellowknife, has filed its own financial analysis of the project with the JRP which suggests that the pipeline would remain economically viable even with no government assistance. The report suggests that the project will yield a 22 per cent rate of return even if capital costs rise 30 per cent over previous estimates.

TransCanada Pipelines is positioning itself to take over the Mackenzie Valley project, should Imperial Oil declared the project uneconomic and walk away.

First Nations Land Claim Settlements and a New Way of Life

There have been a number of land claim agreements in the Northwest Territories since the days of the Berger Inquiry – the Inuvialuit in 1984, the Gwich’in in 1992, the Sahtu in 1994, and the Inuit in the Eastern Arctic through the creation of Nunavut in 1999. The agreements, in various stages of implementation and development, have resulted in aboriginal peoples gaining ownership of land and resources, and having control over resource development. They have ushered in a new way of life for the aboriginal people of the north.

I wish to speak briefly about the Inuvialuit who occupy the Delta, the western part of the Northwest Territories. Since their claim in 1984, they have successfully managed their lands and resources. They have used their monies in appropriate investments and business opportunities. Today, the Inuvialuit are a driving force in the Delta region and western NWT. They have spread their investment tentacles throughout Western Canada. They have invested in all kinds of projects and businesses. They own office buildings. They have an oil and gas exploration company, regional airlines, barging and trucking companies and a multitude of businesses which provide employment for their people and others. In June 1999, the Inuvialuit completed a 30-mile natural gas pipeline from a gas field on their lands to Inuvik which now provides fuel for heating and power production.I noticed in a recent magazine article that the Inuvialuit are offering some lands for oil and gas exploration through a bid process. In 1999, they signed $180 million worth of contracts for exploration work on their lands. The 1998 annual report of the Inuvialuit Regional Corporation, the latest report available, outlines the success of all the various corporations as being $8 million in profit.

The opportunity to join the modern economy has pleased many aboriginal people. They appreciate the chance to become more independent and self-reliant and resent the opposition to the Mackenzie Gas Project from environmentalists. However, many others feel that the project will destroy their traditional way of life and the cultural, social and environmental fabric that they rely on.

The Aboriginal Pipeline Group

The Aboriginal Pipeline Group (APG) was created in 2000 following meetings in Fort Liard and Fort Simpson. Thirty Aboriginal leaders from all regions of the Northwest Territories signed the resolution that created the APG and set its goals. The APG represents the interests of Aboriginal people in the Northwest Territories in maximising the ownership and benefits in a Mackenzie Valley natural gas pipeline.The message that the chiefs and the aboriginal leaders wish to make is that, yes, times have changed. Aboriginal peoples are no longer opposing projects, such as huge gas pipelines traversing their lands. However, they intend to be involved in all aspects of the project – the planning, the route selection, construction and, most important, ownership of the pipeline.

The APG, whose preliminary research costs have been funded through a loan from TransCanada Pipelines, has negotiated a deal by which its ownership of and revenues from the pipeline are to be determined by the amount of gas flowing through it. This does not initially amount to the one third share commonly quoted in the media. At the volume of gas initially expected to flow south – approximately 0.8 bcf per day – the deal would give the APG 3% ownership of the line. The stake would grow to 18% with an increase of 0.2 bcf per day, while an additional 0.4 bcf per day would take the aboriginal share to one third. The success of the deal from the perspective of the APG is therefore heavily dependent on additional exploration and development in the Northwest Territories. The APG is confident that this will occur, but if it does not, the APG could be left with large loans to repay and little means with which to repay them.

The APG will have to repay the TransCanada Pipelines loan, estimated at $140 million, once the regulatory review concludes. With approval of the pipeline and long-term shipping contracts, the APG would be able to borrow the $1.6 billion share of the pipeline construction cost that it would be responsible for. Once gas began to flow, the APG would receive its share of transportation fees, after the operating costs of the pipeline were covered. The APG expects to earn $10-$20 million per year above the cost of repaying the loan for the first twenty years, depending on the quantity of gas flowing. After repayment of the loans, the APG expects to earn up to $120 million per year. These returns are, however, contingent on a risky business prone to boom and bust, especially when energy prices are volatile.

In addition to returns from gas flowing south, the First Nations involved in the APG also expect to benefit considerably from economic development as a result of the pipeline. They anticipate up to 8,600 skilled and unskilled jobs during the construction period, as well as many business opportunities for supplying goods and services to pipeline construction crews and companies. New training programs have been initiated for aboriginal oil service workers in anticipation of these employment opportunities.

Currently, three of the four main aboriginal groups have signed on to the APG – Sahtu, the Gwich’in and the Inuvialuit. Of these, the Sahtu will have a 34% stake in the APG, the Gwich’in a 20% share, and the Inuvialuit a 4% share. The Deh Cho leadership, which would have been allocated a 34% stake, has declined to participate. The remaining 8% has been set aside for other aboriginal groups in the Northwest Territories.

The Deh Cho Holdouts

Grand Chief Herb Norwegian has consistently linked Deh Cho participation in the Mackenzie Gas Project to settlement of their outstanding land claim, which covers 40% of the planned pipeline route. The federal government has made an offer which it describes as “consistent with other agreements that the government of Canada has negotiated over the last 30 years North of 60”. The Deh Cho Dene were offered $104 million and ownership of about 18% of their traditional land, along with surface and mineral titles, but Norwegian called it a “low-ball” offer. Instead, the Deh Cho leadership is seeking a power-sharing agreement over 80,000 square miles of ancestral territory, allowing them to preserve lands for cultural or environmental reasons, to control industrial development and to collect royalties and taxes. However, the chief federal negotiator has refused to contemplate giving 4,500 people the power to govern an area about half the size of France.

Deh Cho leaders have acknowledged that withholding support for the project gives them leverage to secure unprecedented authority, but the federal government appears ready to call their bluff, indicating that they are prepared to authorise the project with or without Deh Cho approval. The Grand Chief has threatened in return to resort to litigation and blockades. Fred Carmichael, chairman of the APG, adding to the game of brinkmanship, has commented:

They are walking on pretty thin ice, because at the end of the day they could end up with no ownership in the pipeline and it could be built without any settlement of their land claim.

The unity of the Deh Cho appears to be crumbling under the pressure, with half the population rejecting the link between land claims talks and joining the APG. Separate Deh Cho groups are now seeking to join the APG in their own right and stand to receive a proportionate share of the 34% ownership reserved for the Deh Cho First Nation as a whole. This group, led by relatives of the Grand Chief, believes political negotiations shouldn’t prevent the Deh Cho Dene from doing business and taking advantage of what they see as an economic opportunity.

Folks are romanticising about when we lived off the land. We are not going back to snowshoes and dog teams.

The group is concerned that aboriginal unemployment in the Territories is double the 5.4% figure for the population as a whole, and that there is no new money coming into the community. They are concerned that their present leadership could repeat the 1980s decision not to take a 10% stake in the Enbridge oil pipeline – a decision which arguably cost the Dene $100 million.

On the other hand, many Deh Cho are afraid that:

…hundreds of trucks would disrupt their quiet communities, that construction camps would breed drug and alcohol abuse, and that the massive project would drive away caribou, moose and other wildlife that sustain people.In the long run, they fear the project would spur a wave of oil and gas prospecting that would bring more pipelines and roads and so many newcomers that the Deh Cho could become a powerless minority in the land they have occupied for many centuries.

A Competing Pipeline

While the Mackenzie Valley pipeline is stalled over land claims, a competing pipeline is being planned in Alaska, where there are proven gas reserves of 30 tcf and total reserves estimated by some at 100 tcf. Alaska’s governor is determined to push for a natural gas pipeline to the Alaskan south coast, with a view to liquefying it for the booming LNG market. The Alaskan pipeline would be longer, and the plans are not as advanced as the Mackenzie Valley pipeline, however, the Canadian government is concerned that the proposed Alaskan pipeline could threaten the future of the Canadian plan. Political pressure could thus be brought to bear on all parties in order to secure a deal.

Pipe-Dreams

Until about seventy years ago, the native peoples of the far north relied on their skills as hunters to feed their families and were self-sufficient. With the extension of Canadian sovereignty northwards, the nomadic people were encouraged to gather in permanent settlements where they could be supplied from the south with food, education and medical care. Settlements, such as those in the Arctic Islands for instance, were often well north of natural food supplies, leaving the inhabitants dependent on a supply route from the south. While fresh food and lightweight goods can be brought in by air or by road, heavy freight such as fuel still depends on the barges that travel in the Mackenzie River during the short summer navigation season. This is a life critically dependent for the necessities of life on the continued availability of fossil fuels.

Click to Enlarge

The town of Norman Wells (pdf warning) in the Sahtu illustrates the difficulties that may befall many northern communities if fossil fuels should become scarce or extremely expensive. The NWT Power Corp will have to use diesel generators to meet the electricity demand for Norman Wells this winter as Imperial Oil’s gas turbines can no longer meet the town’s needs. The local oil field is only expected to last until about 2020, and NWT Power Corp will not commit itself to supplying diesel power beyond this winter. Imperial has been warning the town to begin conserving natural gas since the mid-1990s, but during that time economic activity has increased dramatically and demands on the grid have increased with it. Town officials have done nothing to conserve while supplies were plentiful. Norman Wells is now pinning its hopes on the Mackenzie Valley pipeline, from which it would be able to draw gas supplies, but the pipeline cannot possibly be built in time to prevent a critical situation from developing.

Peak oil and gas could be very cruel to northern communities who came late to modernity and may now have been sold a pipe-dream.

Income Trusts and the Canadian Energy Sector

Finance Minster Jim Flaherty recently gave the income trust sector an unwelcome surprise. Prime Minister Harper had previously promised to “stop the Liberal attack on retirement savings and preserve income trusts by not imposing any new taxes on them”, but the government underestimated the momentum towards trust conversion and was facing a very significant loss of tax revenue.

Not satisfied with merely preventing new trust conversions, Flaherty decided to impose retroactive tax measures on existing trusts. Many of these existing trusts happen to underpin conventional oil and gas production in Alberta – in fact the trust structure was initially developed to facilitate production from mature assets in the oilpatch. The proposed tax changes could therefore have a significant effect on energy production and the Alberta economy specifically. Departing Alberta Premier Ralph Klein welcomed the tax measure.

Alberta was hurt by the trust tax loophole. We were losing hundreds of millions of dollars in revenue.

However, he and the rest of Alberta may well be far less pleased once the implications of this experiment in retroactive tax policy come home to roost. Continue reading “Income Trusts and the Canadian Energy Sector”

Smart Metering and Smarter Metering

Imagine for a moment that we bought food in the way we currently buy electricity. We might order from a supply list with no prices marked and have whatever we fancied delivered to our door whenever we pleased. A single, un-itemized bill would arrive in the mail once every couple of months covering all the food ordered and delivered during the billing period. How would our food bills probably compare to what they are currently? How would we go about reducing our food bill in order to save money when we know nothing about the cost of each act of consumption? If the ‘Ministry of Food Supply’ were worried about the amount of food available, reliance on expensive imports or whether the delivery system might not be up to the task, what could they do to encourage a ‘food conservation culture’?What is missing from our hypothetical scenario is real-time price feedback, which would allow consumers to take responsibility for their own consumption. Its absence makes the task of trying to reduce demand much more difficult, both for consumers and for those trying to manage the supply. If we are ever to introduce a conservation culture, the tradition of passive consumption must first be challenged. Continue reading “Smart Metering and Smarter Metering”