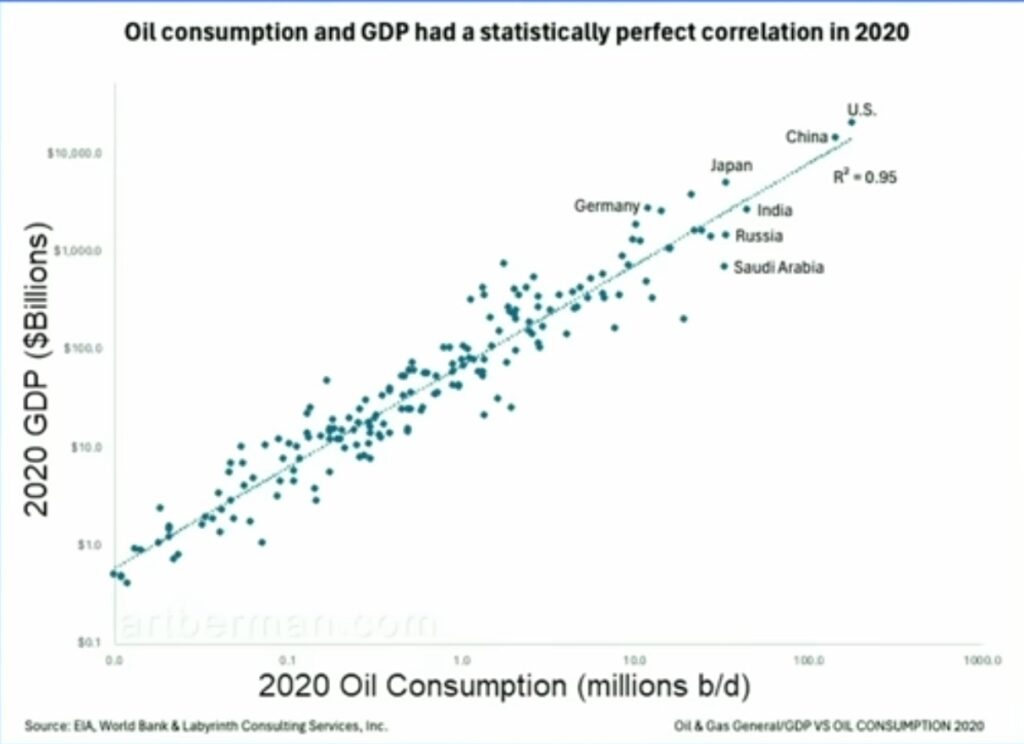

Chris Martenson is an excellent analyst. I strongly suggest following his work, starting with watching the video posted above. The graphs in this post come from the video. Subscribing to his channel, and his online community if you can afford it, is highly recommended. In this presentation, Chris goes through the math of what’s happening with the global oil market, and the implications for the future of the global economy. The picture is stark indeed. GDP is extremely tightly correlated with oil consumption, meaning that as available supply is cut, the economies of countries will be forced into contraction, with some countries faring better than others due to native supplies and refining capacity or lack thereof. Less lucky countries are going to suffer considerably, and in the relatively near future.

Trump has been loudly announcing to the world that they can rely on US oil production to fill the gap, but this could not be further from the truth. The US is a net importer of the long chain hydrocarbons that everyone needs in order to make diesel, kerosene, and bunker fuel. Its normal exports are of short chain hydrocarbons that are not refinery feedstocks and cannot be used to produce these essentials. The US is currently exporting from its own strategic reserve, which is an incredibly short-sighted move. It will not be able to keep this up for long, and when this fails, prices will spike as the futures price, which has been artificially suppressed, and the spot price converge at an eye-watering level. In the meantime, price suppression has encouraged subsidised use, which will deplete available supplies even faster, and hasten the coming price and availability shock. The illusion of normality will die abruptly.

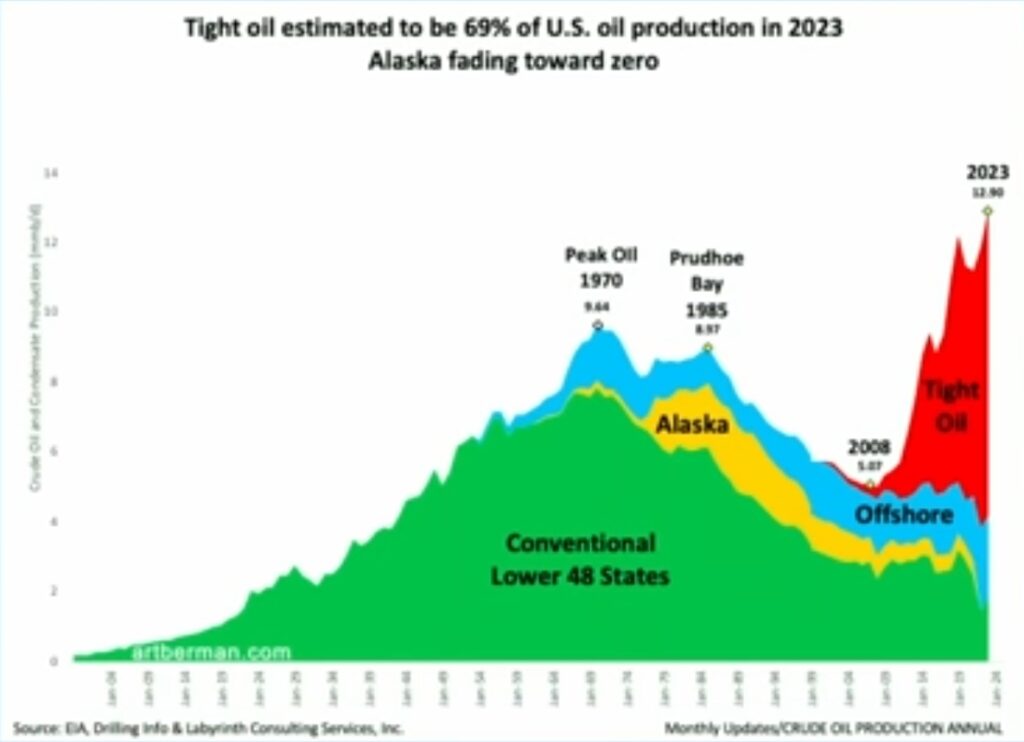

The US has been increasingly relying on tight oil production, since its conventional reserves peaked in the 1970s. However, much of what comes out of these wells is light oil and even shorter chain hydrocarbons. This is the foundation for US exports, and the US must import from places able to produce heavy oil to blend with its own production in order to match the input requirements for their refineries. Refineries are tooled to take a certain blend, and retooling them is extremely expensive. This is why Venezuela was so important to the US, although it will actually take a long time to ramp up any significant level of production for export there. Venezuelan oil is extremely heavy, and would be the perfect companion to American production. Venezuela is also very close to the US, so there would be lower transport costs.

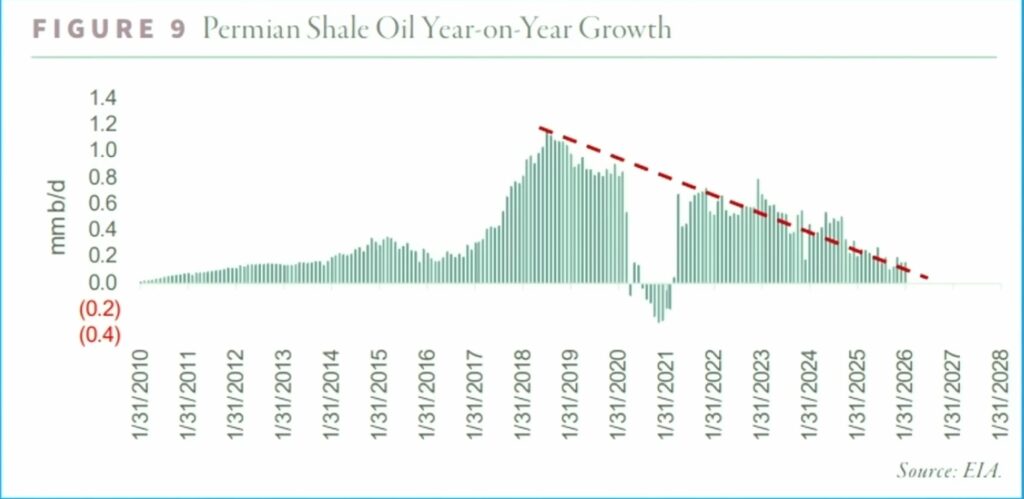

Tight oil has taken off since 2008, but that too is now peaking. All recent growth has been coming from the Permian basin, but that too is now flattening out. This means US oil production is going to go into decline in the relatively near future. Additional drilling will not change this situation, as the sweet spots have already been drilled. Trump is living in fantasy land if he thinks he can do anything about this. Even allowing reserved land to be drilled is not going to make a difference, especially since reserved land tends to be in far flung places with little no existing infrastructure. All of that would have to be built in advance, at great cost in both capital and energy, meaning that no production could arrive before crisis hits, and even then the energy returned over energy invested would likely be very low. This is critical, as it means any new production would result in relatively little of the surplus (above the energy cost of producing more energy) necessary to maintain socioeconomic complexity. Long before any of this could happen, society will have been forced to simplify drastically.

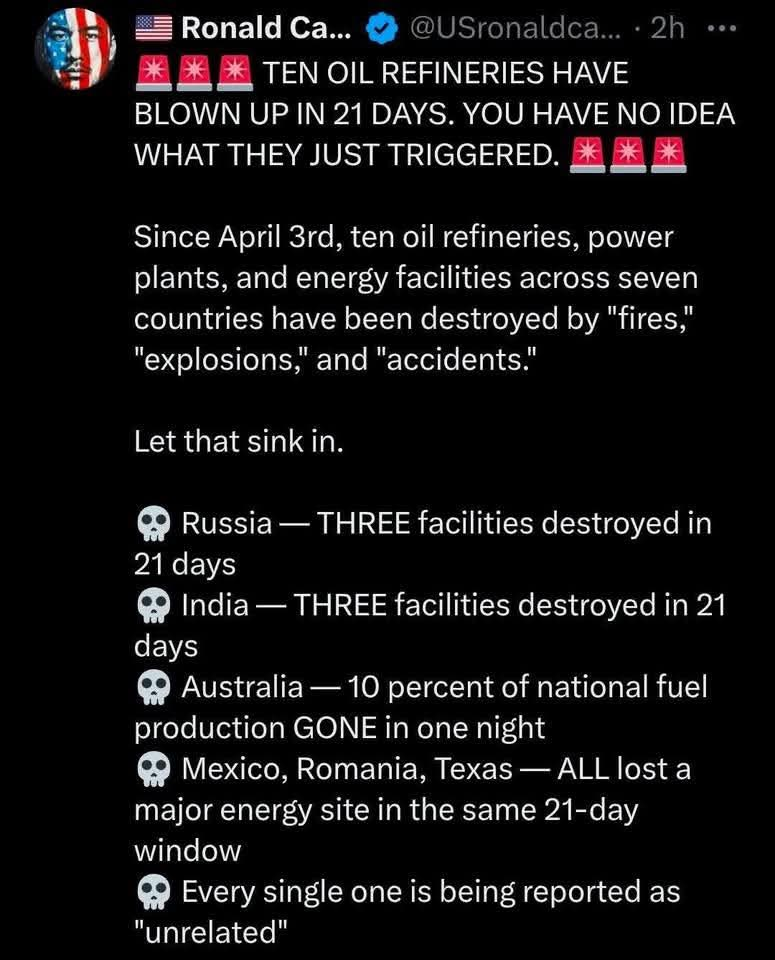

Chris goes into considerable detail as to the impacts of the war in the Gulf. Of course the actual situation will significantly worse, because the war with Iran will not end tomorrow, the war between Russia and Ukraine is also going to have an ongoing impact, and energy infrastructure, such as refineries and storage tanks, is being blown up all over the world with remarkable frequency. It beggars belief to think that these fires and explosions could be coincidental.

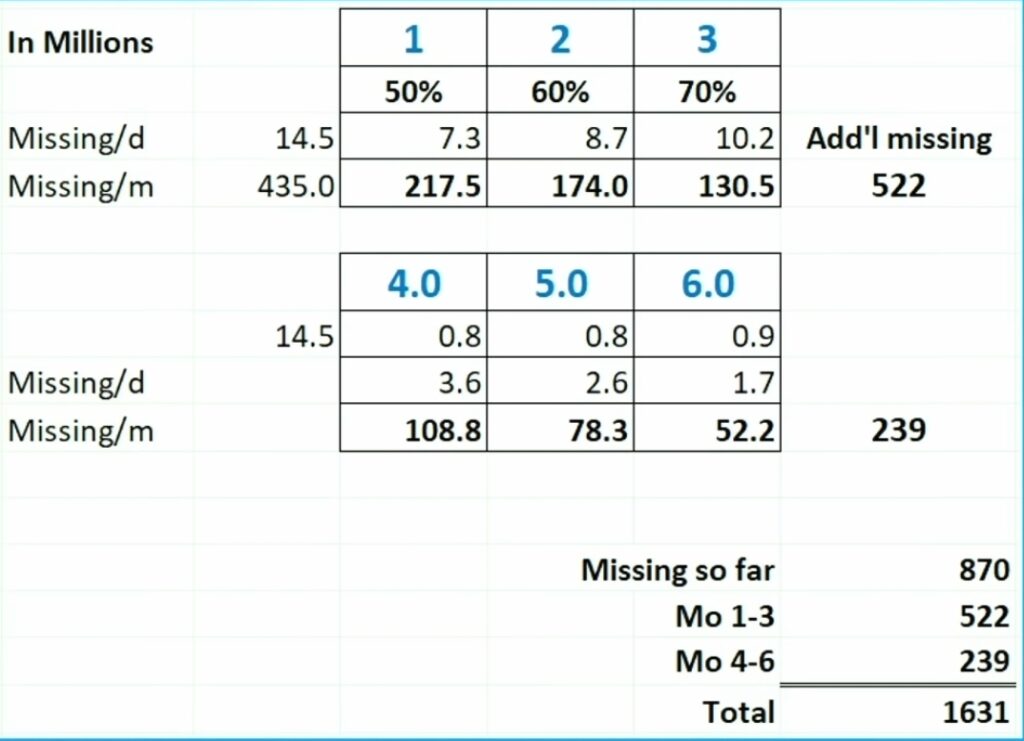

For this reason the math Chris presents is the ultimate best case scenario, although even this would not look like best case to anyone still expecting a return to some semblance of normality. Gulf crude oil production has fallen by 14.5million barrels/day, tanker capacity is down by 50%, and fields have been damaged through necessary production shut-ins. The proportion of oil available for export, as opposed to oil consumed in the countries which produce it, has fallen even further.

The International Energy Agency (IEA) has run the numbers, quoted by Chris, for a scenario where the war stops tomorrow. They project a potential 70% recovery after three months, rising to 88% after six months. The world is currently missing 870million barrels of oil after the two month war. Add to this the inevitable deficits during the modelled recovery, and the missing total would be 1631 million barrels. There is no capacity to make up this lost production. This means a global depression, unevenly distributed, is already baked in the cake, as a best case scenario.

Refiners are currently working with their commercial reserves, which cannot fall below a critical level in order to keep oil flowing smoothly through the facility without sucking in air or sludge from the bottom of a tank. That critical minimum level is now being reached. As for strategic reserves, the total available for the four largest holders combined is about half of the number of missing barrels to date.

A critical theshhold has been reached. If the disruption to supplies doesn’t end very soon, the global damage will be catastrophic, and the associated death rate will be appalling. People have no idea what’s about to hit them. Everyoneneeds to wake up and come together to help each other to survive this.